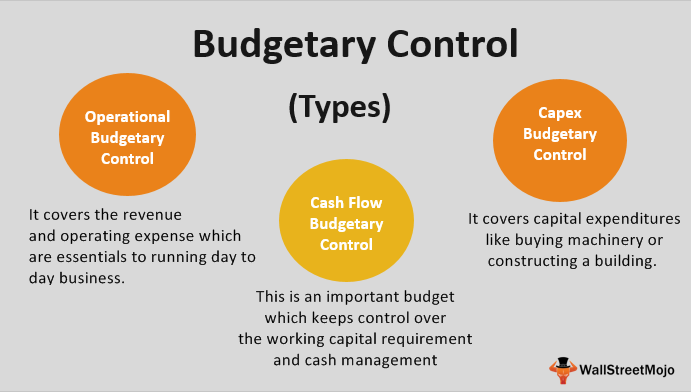

What is budgetary control?

Budgetary

control is the

process by which budgets are prepared for the future period and are compared

with the actual performance for finding out variances, if any. The comparison

of budgeted figures with actual figures will help the management to find out

variances and take corrective actions without any delay.

Objectives of Budgetary Control

The main

objectives of budgetary control are given below:

1. Defining the

objectives of the enterprise.

2. Providing plans

for achieving the objectives so defined.

3. Coordinating

the activities of various departments.

4. Operating

various departments and cost centres economically and efficiently.

5. Increasing

profitability by eliminating waste.

6. Centralizing

the control system.

7. Correcting

variances from sit standards.

8. Fixing the

responsibility of various individuals in the enterprise.

Advantages of Budgetary Control

Budgetary control

has become an important tool of an organization to control costs and to

maximize profits. Some of the advantages of budgetary control are:

1. It defines the

goals, plans and policies of the enterprise. If there is no definite aim then

the efforts will be wasted in achieving some other aims.

2. Budgetary

control fixes targets. Each and every department is forced to work efficiently

to reach the target. Thus, it is an effective method of controlling the

activities of various departments of a business unit.

3. It secures

better co-ordination among various departments.

4. In case the

performance is below expectation, budgetary control helps the

management in finding up the responsibility.

5. It helps in

reducing the cost of production by eliminating the wasteful expenditure.

6. By promoting

cost consciousness among the employees, budgetary control brings in

efficiency and economy.

7. Budgetary

control facilitates centralized control with decentralized activity.

8. As everything

is planned and provided in advance, it helps in the smooth running of business

enterprise.

9. It tells the

management as to where the action is required for solving problems without delay.

Disadvantages or Limitations of Budgetary Control

The following are

the limitations of budgetary control:

1. It is really

difficult to prepare the budgets accurately under inflationary conditions.

2. Budget involves

a heavy expenditure which small business concerns cannot afford.

3. Budgets are

prepared for the future period which is always uncertain. In future, conditions

may change which will upset the budgets. Thus, future uncertainties minimize

the utility of a budgetary control system.

4. Budgetary

control is only a management tool. It cannot replace management in

decision-making because it is not a substitute for management.

5. The success of

budgetary control depends upon the support of the top management. If there is

lack of support from top management, then this will fail.

Comments

Post a Comment