1.1 - Introduction, Definition, Silent Features of Company, Act 2013

Introduction:

The Indian Companies Act 1956 has been

replaced by the Indian Companies Act, 2013. The Companies Act 2013 makes

complete provisions to govern all listed and unlisted companies in the country.

The Companies Act 2013 introduced several new Sections and repealed the

Relevant Corresponding Sections of the Companies Act 1956. This Act is considered

a Landmark Legislation.

Key Highlights of the Indian Companies Act 2013

Maximum Number of Members (Shareholders)

for a Private Limited Company is increased from 50 to 200.

One-Person Company

Section 135 of the Act deals with

Corporate Social Responsibility

Company Law Tribunal and Company Law

Appellate Tribunal.

Salient

Features of the Companies Act 2013

It has introduced the concept

of ‘Dormant Companies’. Dormant companies are those that have not engaged in

business for two years consecutively.

It introduced the National Company Law Tribunal. It is a quasi-judicial body in India adjudicating

issues concerning companies. It replaced the Company Law Board.

It provides for

self-regulation with respect to disclosures and transparency rather than having

a government-approval based regime.

Documents have to be

maintained in electronic form.

Official liquidators have

adjudicatory powers for companies having net assets of up to Rs.1 crore.

The procedure for mergers and

amalgamations have been made faster and simpler.

Cross-border mergers are

allowed by this Act (foreign company merging with an Indian company and reverse)

but with the permission of the Reserve Bank of India.

The concept of a one-person

company has been introduced. This is a new type of private company that may

have only one director and one shareholder. The 1956 Act required at least two

directors and two shareholders for a private company.

Having independent directors

has been made a statutory requirement for public companies.

For a prescribed class of

companies, women directors are mandatory.

All companies should have at

least one director who has been a resident of India for not less than 182 years

in the last calendar year.

The Act provides for

entrenchment (apply extra-legal safeguards) of the articles of association.

The Act mandates at least 7

days of notice for calling board meetings.

In this Act, the duties of a

Director has been defined. It has also defined the duties of ‘Key Managerial

Personnel’ and ‘Promoter’.

For public companies, there

should be a rotation of audit firms and auditors. The Act also prevents auditors

from performing non-audit services to the company. In case of non-compliance,

there is substantial criminal and civil liability for an auditor.

The whole process of

rehabilitation and liquidation of the companies in the case of the financial crisis

has been made time-bound.

The Act makes it mandatory for

companies to form CSR committees, and formulate CSR policies. For certain

companies, mandatory disclosures have been made with regard to CSR.

Listed companies ought to have

one director to represent small shareholders as well.

There is provision for search

and seizure of documents, during the investigation, without an order from a

magistrate.

Norms have been made stringent

for accepting deposits from the public.

Setting up of the National

Financial Reporting Authority (NFRA) has been provided for. It engages in the

establishment and enforcement of accounting and auditing standards and

oversight of the work of auditors. (Due to notification of NFRA, India is now

eligible for membership of the International Forum of Independent Audit

Regulators (IFIAR).)

The Act bans key managerial

personnel and directors from purchasing call and put options of shares of the

company, if such person is reasonably expected to have access to

price-sensitive information.

The Act offers more power to

shareholders in that it provides for shareholders’ approval for many major

transactions.

1.2 Formation of Company, Stages of Formation

Formation of COMPANIES

The formation of a company is

a lengthy process. For convenience, the whole process of company formation may

be divided into the following four stages: 1. Promotion Stage 2. Incorporation

or Registration Stage 3. Capital Subscription Stage 4. Commencement of Business

Stage.

Stage # 1. Promotion Stage:

Promotion is the first stage in

the formation of a company. The term ‘Promotion’ refers to the aggregate of

activities designed to bring into being an enterprise to operate a business. It

presupposes the technical processing of a commercial proposition with reference

to its potential profitability. The meaning of promotion and the steps to be

taken in promoting a business are discussed in brief here.

Promotion of a company refers

to the sum total of the activities of all those who participate in the building

of the enterprise up to the organisation of the company and completion of the

plan to exploit the idea. It begins with the serious consideration given to the

ideas on which the business is to be based.

According to C.W. Grestembeg,

“Promotion may be defined as the discovery of business opportunities and the

subsequent organisation of funds, property and managerial ability into a

business concern for the purpose of making profits therefrom.”

According to H.E. Heagland,

“Promotion is the process of creating a specific business enterprise. Its scope

is very broad, and numerous individuals are frequently asked to make their

contributions to the programme. Promotion begins when someone gives serious

consideration to the formulation of the ideas upon which the business in

question is to be based. When the corporation is organised and ready for

operation, the major function of promotion comes to an end.”

According to Guthmann and

Dougall, “Promotion starts with the conception of the idea from which the

business is to evolve and continues down to the point at which the business is

full, ready to begin operations in a going concern.”

Stage # 2. Incorporation or Registration Stage:

Incorporation or registration

is the second stage in the formation of a company. It is the registration that

brings a company into existence. A company is properly constituted only when it

is duly registered under the Act and a Certificate of Incorporation has been

obtained from the Registrar of Companies.

Procedure to Get a Company Registered:

In

order to get a company registered or incorporated, the following procedure is

to be adopted:

(A)

Preliminary Activities:

Before

a company is incorporated, the promoter has to take a decision regarding the

following:

1. To decide the name of the

company

2. Licence under Industries Development

and Regulation Act, 1951

(B)

Filing of Document with the Registrar:

1. Memorandum of Association

2. Articles of Association

3. List of directors

4. Written consent of

directors

5. Statutory declaration

Certificate

of Incorporation:

On the registration of

memorandum and other documents, the Registrar will issue a certificate known as

the Certificate of Incorporation certifying under his hand that the company is

incorporated and, in the case of a limited company that the company is limited.

The specimen

of the certificate of incorporation is given below:

Effects

of Incorporation:

The

certificate of incorporation is conclusive evidence of the fact that:

(i) The company is properly

incorporated and duly registered;

(ii) The terms of the

Memorandum and Articles are within the law;

(iii) All requirements of the

Act in respect of registration have been complied with;

(iv) A private company can

start its business after getting the certificate of incorporation; and

(v) With the issue of

certificate, the company takes birth with a separate legal entity.

Stage # 3. Capital Subscription Stage:

A private company or a public

company not having share capital can commence business immediately on its

incorporation. As such ‘capital subscription stage’ and ‘commencement of

business stage’ is relevant only in the case of a public company having a

share capital. Such a company has to pass through these additional two stages

before it can commence business.

Under the capital subscription

stage comes the task of obtaining the necessary capital for the company.

For

this purpose, soon after the incorporation, a meeting of the Board of Directors

is convened to deal with the following business:

1. Appointment of the

Secretary. In most cases, the appointment of pre-team secretary (who is

appointed at the promotion stage) is confirmed.

2. Appointment of bankers,

auditors, solicitors and brokers, etc.

3. Adoption of draft

‘prospectus’ or ‘statement in lieu of prospectus’.

4. Adoption of underwriting

contract, if any.

Besides

the above-mentioned business, the Board also decides as to whether:

(i) a public offer for capital

subscription is to be made, and

(ii) Listing of shares at a

stock exchange is to be secured.

The company will now proceed

to obtain the permission of the Controller of Capital Issue, New Delhi, under

the Capital Issue Control Act, 1947 if a public offer for sale of shares and

debentures exceeding Rs. one crore is to be made during a period of 12 months,

unless the issue fulfils the conditions of exemption as laid down in the

Capital Issue (Exemption) Order, 1969.

The Capital Issue Control Act,

1947 however, does not apply to a private company, a banking company, an

insurance company and a government company provided it does not make an issue

of securities to the general public.

After the above formalities

have been completed, the directors of the company file a copy of the

‘prospectus’ with the Registrar and invite the public to subscribe to the shares of

the company by putting the ‘prospectus’ in circulation.

Application for shares are

received from the public through the company’s bankers and if the subscribed

capital is at least equal to the minimum subscription amount as disclosed in

the prospectus and other conditions of a valid allotment are fulfilled, the

directors of the company pass a formal resolution of allotment.

Allotment letters are then

posted, the return of allotment is filed with the Registrar and share certificates

are issued to the allottees in exchange of the allotment letters. If the

subscribed capital is less than the minimum subscription or the company could

not obtain the minimum subscription within 120 days of the issue of the prospectus,

all money will be refunded and no allotment can be made.

It may be noted that a public

a company having a share capital, but not issuing a ‘prospectus’ has to file with

the Registrar ‘a Statement in lieu of Prospectus’ at least three days before

the directors proceed to pass the first allotment resolution.

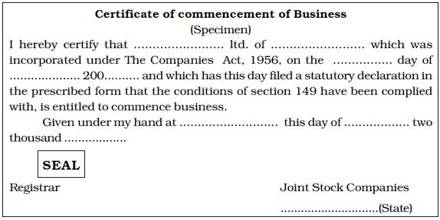

Stage # 4. Commencement of Business Stage:

After getting the certificate

of incorporation, a private company can start its business. A public company

can start its business only after getting a’ certificate of commencement of

business’.

After

getting the certificate of incorporation:

(i) A public company issues a prospectus

of inviting the public to subscribe to its share capital,

(ii) A minimum subscription is

fixed, and

(iii) The company is required

to sell a minimum number of shares mentioned in the prospectus.

After making the sale of the

required number of shares a certificate is sent to the Registrar stating this

fact, along with a letter from the banks, that it has received an application

money for such shares.

The Registrar scrutinizes the

documents. If he is satisfied, then issues a certificate known as Certificate

of Commencement of Business. This is the conclusive evidence of the

commencement of the business.

The

specimen of a certificate of commencement of business is given below:

1.3 Promoters, Function of Promoter, Duties & Liabilities of Promoter

PROMOTERS

Meaning

of a Promoter:

The idea of carrying on a

business which can be profitably undertaken is conceived either by a person or

by a group of persons who are called promoters. After the idea is conceived,

the promoters make detailed investigations to find out the weaknesses and

strong points of the idea, to determine the amount of capital required and to

estimate the operating expenses and probable income.

The term ‘promoter’ is a term

of business and not of law. It has not been defined anywhere in the Act, but a

number of judicial decisions have attempted to explain it.

ADVERTISEMENTS:

According to L.J. Brown. “The

term promoter is a term not of law but of business, usefully summing up in a

single word a number of business operations familiar to the commercial world by

which a company is generally brought into existence.”

According to Justice C.

Cockburn. “Promoter is one who undertakes to form a company with reference to a

given object and to set it going, and who takes the necessary steps to accomplish

that purpose.”

According to Palmer, “Company

promoter is a person who originates a scheme for the formation of the company,

has the memorandum and the articles prepared, executed and registered and finds

the first directors settle the terms of preliminary contracts and prospectus

(if any) and makes arrangement for advertising and circulating the prospectus

and placing the capital.”

According to Guthmann and

Dougall. “Promoter is the person who assembles the men, the money and the

materials into a going concern.”

From

these definitions of promoter it is concluded that:

“Promoter is the person who

originates the idea for the formation of a company and gives the practical shape to

that idea with the help of his own resources and with that of others.”

A person cannot be held as

promoter merely because he has signed at the foot of the Memorandum or that he

has provided money for the payment of formation expenses.

The promoters, in fact, render

a very useful service in the formation of the company. A promoter has been

described as ”a creator of wealth and an economic prophet.” The promoters carry

a considerable risk because if the idea sometimes goes wrong then the time and

money spent by them will be a waste.

In the words of Henry E.

Heagland, “A successful promoter is a creator of wealth. He is an economic

prophet. He is able to visualise what does not yet exist and to organise

business enterprise to make the products available to the using public.”

A promoter may be an individual,

a firm, an association of persons or even a company.

Functions

of a Promoter:

The

Promoter Performs the following main functions:

1. To conceive an idea of

forming a company and explore its possibilities.

2. To conduct the necessary

negotiation for the purchase of a business in case it is intended to purchase an

existing business. In this context, the help of experts may be taken, if

considered necessary.

3. To collect the requisite

number of persons (i.e. seven in case of a public company and two in case of a

private company) who can sign the ‘Memorandum of Association’ and ‘Articles of

Association’ of the company and also agree to act as the first directors of the

company.

4. To decide about the

following:

(i) The name of the Company,

(ii) The location of its

registered office,

(iii) The amount and form of

its share capital,

(iv) The brokers or

underwriters for a capital issue, if necessary,

(v) The bankers,

(vi) The auditors,

(vii) The legal advisers.

5. To get the Memorandum of

Association (M/A) and Articles of Association (A/A) drafted and printed.

6. To make preliminary

contracts with vendors, underwriters, etc.

7. To make arrangement for the

preparation of the prospectus, it's filing, advertisement and issue of capital.

8. To arrange for the

registration of the company and obtain the certificate of incorporation.

9. To defray preliminary

expenses.

10. To arrange the minimum

subscription.

Duties

of Promoter:

The

duties of promoters are as follows:

1.

To disclose the secret profit:

The promoter should not make

any secret profit. If he has made any secret profit, it is his duty to disclose

all the money secretly obtained by way of profit. He is empowered to deduct the

reasonable expenses incurred by him.

2.

To disclose all the material facts:

The promoter should disclose

all the material facts. If a promoter contracts to sell the company a property

without making a full disclosure, and the property was acquired by him at a

time when he stood in a fiduciary position towards the company, the company may

either repudiate the sale or affirm the contract and recover the profit made

out of it by the promoters.

3.

The promoter must make good to the company what he has obtained as a trustee:

A promoter stands in

fiduciary position towards the company. It is the duty of the promoter to make

good to the company what he has obtained as trustee and not what he may get at

any time.

4.

Duty to disclose private arrangements:

It is the duty of the promoter

to disclose all the private arrangement resulting in him profit by the promotion

of the company.

5.

Duty of promoter against the future allottees:

When it is said the promoters

stand in a fiduciary position towards the company then it does not mean that

they stand in such relation only to the company or to the signatories of

memorandums of the company and they will also stand in this relation to the future

allottees of the shares.

Liabilities

of Promoter:

The

liabilities of promoters are given below:

1.

Liability to account in profit:

As we have already discussed

that promoter stands in a fiduciary position to the company. The promoter is

liable to account to the company for all secret profits made by him without

full disclosure to the company. The company may adopt any one of the following

two courses if the promoter fails to disclose the profit.

(i)The company can sue the

promoter for an amount of profit and recover the same with interest.

(ii) The company can rescind

the contract and can recover the money paid.

2.

Liability for mis-statement in the prospectus:

Section 62(1) holds the

promoter liable to pay compensation to every person who subscribes for any

share or debentures on the faith of the prospectus for any loss or damage

sustained by reason of any untrue statement included in it. Sec. on 62 also

provides certain grounds on which a promoter can avoid his liability. Similarly

Sec. 63 provides for criminal liability for mis-statement in the prospectus and

a promoter may also become liable under this section.

The promoter may also be

imprisoned for a term which may extend to two years or maybe punished with the

fine up to Rs. 5,000 for untrue statements in the prospectus. (Sec. 63).

3.

Personal liability:

The promoter is personally

liable for all contracts made by him on behalf of the company until the

contracts have been discharged or the company takes over the liability of the

promoter.

The death of the promoter does not

relieve him from liabilities.

4.

Liability at the time of winding up of the company:

In the course of winding up of

the company, on an application made by the official liquidator, the court may

make a promoter liable for misfeasance or breach of trust. (Sec. 543).

Further, where fraud has been

alleged by the liquidator against a promoter, the court may order for his

public examination. (Sec. 478).

1.4 Types of Company

Different Types of Companies

Companies can be classified into different

types based on their mode of incorporation, the liability of the members, and the number of the members. The most common types of companies are:

- Royal Chartered Companies

- Statutory Companies

- Registered or Incorporated Companies

- Companies Limited By Shares

- Companies Limited By Guarantee

- Unlimited Companies

- Public Company (or Public Limited Company)

- Private Company (or Private Limited Company)

- One Person Company

Types Of Companies Based On The Mode of Incorporation

Companies can be classified into three

types based on whether they are created by a special act, special order, or are

registered just like any normal company.

Royal Chartered

Companies

Royal Chartered Companies are companies

created by the Royal Charter. This means they are granted power or a right by

the monarch or by special order of a king or a queen. Examples of Royal

Chartered Companies are East India Company, BBC, Bank Of England, etc.

Statutory Companies

Statutory Companies are companies

incorporated by means of a special act passed by the central or state

legislature. They are mostly invested with compulsory powers and are

responsible to carry out some special business of national importance. Some

examples of statutory companies are The Reserve Bank of India (formed

under RBI act, 1934), Life Insurance Corporation of India (formed under LIC

Act, 1956).

Registered Or

Incorporated Companies

All the other companies which are incorporated

under the companies' act passed by the government comes under this head. These

companies come under existence only after they register themselves under

the act and the certificate of incorporation is passed by the Registrar of

companies. Google India Pvt Ltd is an example of incorporated companies.

Types Of Companies Based On The Number Of Members

Public Limited

Company

The legal existence of a Public Limited

Company is separate from its members (shareholders) and the liability of its

members is also limited. Its existence is thus not affected by the retirement

or death of its shareholders. A minimum of 7 members is needed to form a Public

Limited company but there is no maximum limit on this. The company collects its

capital by the sale of its shares to the shareholders. The shareholders of a

company do not have the right to participate in the day-to-day management of

the company, thus separating ownership from management. All the major decisions

of the company are taken by the Board of Directors.

Private Limited

Company

Private Limited (Pvt Ltd) companies have

more than 2 and less than 50 members and their liability is limited or

unlimited depending on the type of the company it is. Unlike Public Limited

companies, here the transfer of shares is limited to its members and the

general public cannot subscribe to its shares and debentures. Pvt Ltd companies

are exempted from many rules and regulations which are applicable to Public

Limited companies, for example, the need to file a prospectus with the Registrar,

the need to hold the statutory general meeting or maintain annual reports, etc.

Also, it can start operations after receiving just the certificate of

incorporation, whereas a Public Limited company needs a certificate of

commencement as well. It is a great option if you want the advantages of

limited liability and yet want greater control over your business and maintain

its privacy. This is the most popular type of company for start-ups to be

registered as.

One Person Company

One Person Company (OPC) as a company type

was introduced in the Companies Act of 2013 in India. It is similar to a sole

proprietorship but the owner shall have limited liability and thus his personal

assets would not be at risk of losses need to be recovered or if the company is

liquidated.

Types of Companies Based On The Liability Of The Members

In case of liquidation, the members of a

company can either be liable to pay even from their personal assets or to the

extent of the face value of shares held by them. It all depends on how the

company is registered as. Companies can be classified into three types based on

the liability of the members. These are –

Companies Limited By

Shares

The liability of the shareholders is

limited to the extent of the face value of shares held by them. Most Pvt Ltd

companies are of this type.

Companies Limited By

Guarantee

In these companies, in case of

liquidation, the shareholders promise to pay a certain fixed amount to cover

the liabilities of the company.

Unlimited Companies

There is no limit on the liability of the

shareholders. In case of liquidation, they might have to pay even from their

personal assets to cover the liabilities of the company. This type of company

is quite uncommon today due to obvious reasons.

There are a lot of options to choose from

when you plan to register your startup. Make sure you research the pros and

cons of each and register your firm accordingly. Now that you know about

different types of companies, let’s move on to the guide on how to register your company.

Video

Lecture Links:

Comments

Post a Comment